Published March 25, 2025

Don’t Let Rising Insurance Rates Catch You Off Guard

.png)

Rising Insurance Rates: What Homeowners and Investors Need to Know

When you’re buying a home or investing in real estate, homeowner’s insurance isn’t just a formality — it’s essential protection for your property, your belongings, and your financial future.

And lately? That protection has been getting more expensive.

Whether you're settling into your first home or expanding your rental portfolio, here’s what you need to know about rising insurance rates — and what you can do about them.

Why Homeowner’s Insurance Is Non-Negotiable

Homeowner’s insurance gives you peace of mind and financial backup when the unexpected happens. It typically covers things like repairs or rebuilding after damage from fire, storms, or other covered events. It can also cover your personal belongings — furniture, electronics, clothing — if they’re stolen or damaged. And if someone gets injured on your property, liability protection can help cover medical or legal costs.

For rental properties, landlord insurance works similarly — but with added protections like loss of rental income and tenant-related liability.

What’s Driving Insurance Rates Up?

In recent years, both homeowners and landlords have seen premiums rise, and it’s not random. There are four main reasons behind the increase:

-

More frequent and severe weather events — wildfires, hurricanes, floods, and deep freezes are leading to more (and bigger) claims.

-

Rising construction and repair costs — inflation, supply chain issues, and labor shortages are driving up what it takes to fix or rebuild.

-

Insurance companies are scaling back — some are pulling out of high-risk areas entirely, which reduces options and increases premiums.

-

Claims are outpacing rate increases — insurers are catching up after years of underpricing coverage compared to the cost of claims.

Rental properties are especially impacted. Insurers tend to view them as higher risk due to potential tenant damage, longer vacancy periods, or inconsistent maintenance — which can drive premiums even higher in certain areas.

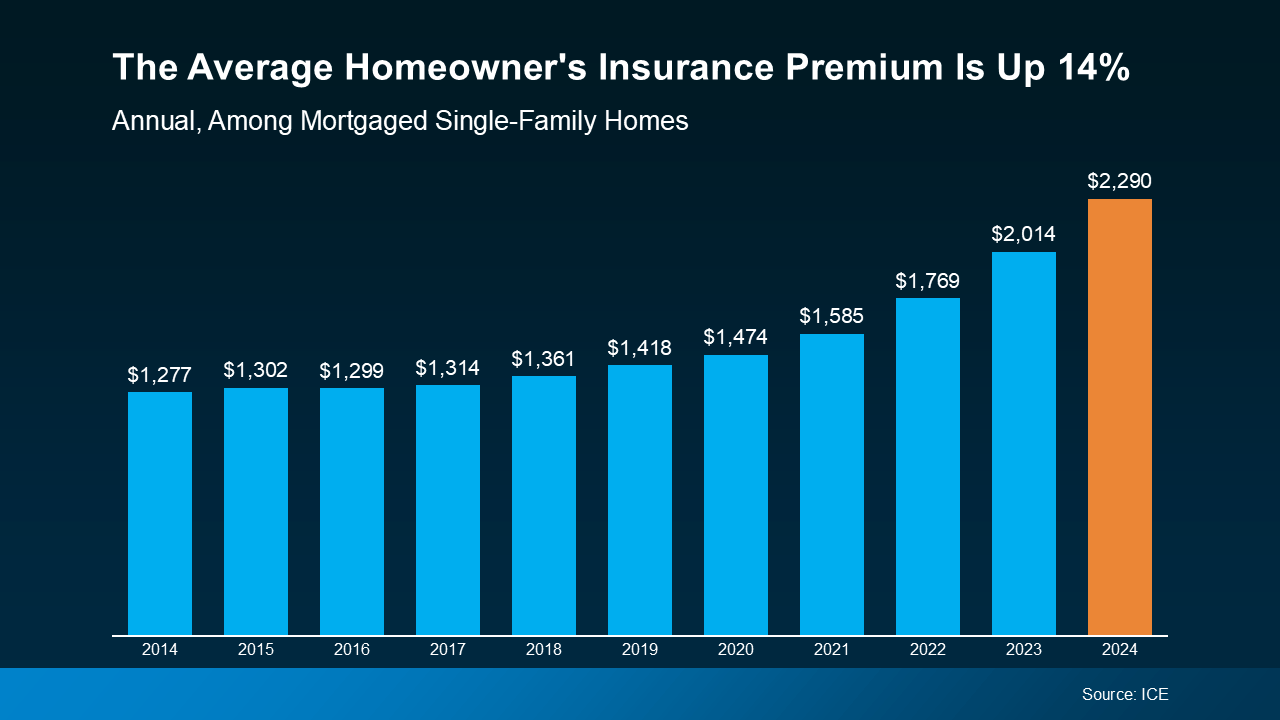

How Much Are Rates Increasing?

According to data from Insurance.com and ICE Mortgage Technology, average yearly premiums have climbed steadily over the past decade. In many states, homeowners are seeing double-digit increases year-over-year. Areas prone to natural disasters or with limited insurer options tend to feel it the most.

What You Can Do to Keep Costs Manageable

You may not be able to stop premiums from rising across the board, but you can take steps to manage your own insurance costs. Start by shopping around — prices vary widely from one company to another. Ask about bundling discounts if you combine policies like home and auto. Installing smart security systems, upgrading your roof, or keeping up with regular maintenance can also reduce risk and help lower your premium.

Review your policy annually to make sure your coverage reflects today’s rebuilding costs and your personal needs — especially if you’ve renovated, added value, or experienced changes to your property.

A First in the Market

Here’s something I’ve never seen in my career — until now. Buyers are starting to include contingencies in their offers that are subject to obtaining satisfactory homeowner’s insurance.

What does that actually mean? It’s similar to a home inspection contingency. The buyer gets a quote for insurance, reviews it, and if the premium feels too high or the coverage too limited, they can walk away from the deal — no questions asked.

It’s a new layer of protection for buyers in today’s market, and honestly, a sign of the times. With premiums rising and insurers tightening their guidelines, buyers are more cautious — and they’re using contingencies to make sure they’re not stepping into a financial surprise after closing.

It’s just one more way the insurance landscape is changing the real estate game in real time.

Bottom Line

Homeowners’ and landlord insurance are essential parts of protecting your investment — but they’re also budget items that are on the rise. As you plan for a new home or add to your real estate portfolio, it’s important to think beyond just your mortgage payment. Your insurance costs matter, and with the right strategy, you can protect your property and your wallet.

|

or another way